Table of Contents

A world economic system already contending with raging inflation, stock-market turmoil and a grueling struggle is dealing with yet one more risk: the unraveling of a large housing growth.

As central banks across the globe quickly improve rates of interest, hovering borrowing prices imply individuals who had been already stretching to purchase property are lastly reaching their limits. The consequences are being seen in international locations corresponding to Canada, the US and New Zealand, the place once-hot residential actual property markets have out of the blue turned chilly.

It’s a pointy reversal from years of surging costs fueled by rock-bottom mortgage charges and authorities stimulus, together with a pandemic that popularized distant work and despatched homebuyers on the hunt for greater areas. An evaluation by Bloomberg Economics exhibits that 19 OECD international locations have mixed price-to-rent and residential price-to-income ratios which can be larger at present than they had been forward of the 2008 monetary disaster — a sign that costs have moved out of line with fundamentals.

Taming frothy house costs are a key a part of many coverage makers’ objectives as they search to quell the quickest inflation in a long time. However as markets shudder from the prospects of a worldwide recession, a slowdown in housing may create a ripple impact that will deepen an financial stoop.

Falling house costs would erode family wealth, dent shopper confidence and probably curb future growth. Animal spirits are usually tamed when persons are confronted with larger compensation prices on an asset that’s shedding worth. And property building and gross sales are enormous multipliers of financial exercise world wide.

“The hazard is enterprise and monetary cycles turning down concurrently, which may result in longer-lasting recessions,” stated Rob Subbaraman, head of worldwide markets analysis at Nomura Holdings Inc. “A decade of QE has fueled frothy housing markets and we may very well be coming into the opposite aspect of this quickly, as housing affordability is stretched and debt-service ratios may rise sharply.”

Such a state of affairs would gum up financial institution lending as the danger of unhealthy loans will increase, choking the move of credit score that economies thrive on. Within the US and Western Europe, the housing crash that precipitated the monetary disaster hobbled banking methods, governments and shoppers for years.

To make certain, a 2008-style collapse is unlikely. Lenders have tightened requirements, family financial savings are nonetheless sturdy and plenty of international locations nonetheless have housing shortages. Labor markets are additionally robust, offering an necessary buffer.

“Decrease costs may have a direct impact on shopper spending and the entire economic system, as usually actual property makes up a major a part of households’ wealth,” stated Tuuli McCully, head of Asia-Pacific economics at Scotiabank. “Nonetheless, as family stability sheets in many main markets stay wholesome, I’m not significantly fearful about dangers associated to accommodate costs and the world economic system.”

Nonetheless, the danger of a pointy drop in costs is clearly higher when there’s a synchronized world tightening of financial coverage, stated Niraj Shah of Bloomberg Economics in London. Greater than 50 central banks have raised rates of interest by not less than 50 foundation factors in a single go this 12 months, with extra hikes anticipated. Within the US, the Federal Reserve final week boosted its major rate of interest by 75 foundation factors, its greatest improve since 1994.

Housing markets in New Zealand, the Czech Republic, Australia and Canada rank among the many world’s bubbliest and are significantly weak to falling costs, in response to Bloomberg Economics. Portugal is particularly in danger within the euro space, whereas Austria, Germany and the Netherlands are also wanting frothy.

In Asia, South Korea home costs additionally look weak, in response to an evaluation by S&P World Rankings. That report famous dangers from family credit score relative to nominal GDP, the expansion charge of family debt and the velocity of house-price good points. Elsewhere in Europe, Sweden has seen a dramatic turnaround in housing demand, sparking concern in a rustic the place debt runs at 200 per cent of family revenue.

Goldman Sachs Group Inc. economists wrote in a report final week that the indicators from house gross sales usually precede costs by about six months, indicating that a number of international locations are more likely to see additional declines in values. A considerable cooldown in housing markets is a crucial cause why developed economies will seemingly sluggish, in response to the economists led by Jan Hatzius.

“The very fast deterioration in affordability and enormous drops in house gross sales counsel {that a} exhausting touchdown is a significant danger, particularly in New Zealand, Canada, and Australia, though that’s not our baseline given present tightness,” the Goldman economists wrote.

Central banks are issuing warnings of their very own. The Financial institution of Canada stated this month in its annual assessment of the monetary system that prime ranges of mortgage debt are of explicit concern as rates of interest rise and extra debtors are strained to pay payments. The Reserve Financial institution of New Zealand’s semi-annual Monetary Stability Report stated that the general risk to the monetary system is proscribed, however a “sharp” decline in home costs is feasible, which may considerably cut back wealth and result in a contraction in shopper spending.

“As borrowing prices rise, actual property markets face a important take a look at,” Bloomberg’s Shah stated. “If central bankers act too aggressively, they might sow the seeds of the following disaster.”

Here’s what’s unfolding in bubbly housing markets world wide.

NEW ZEALAND

If 2021 was the 12 months New Zealand’s house-price progress reached dizzying heights, with an annual improve of near 30 per cent, 2022 is shaping as much as be the 12 months the music stops — and the abrupt change has left folks scrambling.

In March, Jonathan Milne determined it was time to promote a household house within the Auckland suburb of Onehunga and buy a bigger home close by for NZ$2 million (US$1.3 million). He and his spouse, Georgie, had been optimistic of a speedy sale and a superb value for his or her outdated house, which was valued by the native authorities at NZ$1.8 million.

All that modified in April when the RBNZ took aggressive motion to sort out inflation, mountain climbing the official charge by 50 foundation factors to 1.5 per cent — its greatest improve in 22 years. It shortly adopted with one other 50-basis-point bounce in Could and a projection for the speed to peak at near 4 per cent subsequent 12 months.

Milne’s home was meant to be bought in Could through public sale, a preferred methodology of house gross sales in New Zealand, however not a single bidder confirmed up for the occasion.

“What we didn’t anticipate was that it might be so exhausting to market and promote our home,” stated Milne, the 47-year-old managing editor of a information web site. “We knew that each week that handed would knock one other NZ$100,000 off the value.”

On the finish of final month, they accepted a suggestion that Milne described as “dramatically” beneath the federal government valuation.

Economists count on New Zealand home costs will fall about 10 per cent this 12 months and will finally drop as a lot as 20 per cent from their late 2021 peak. Whereas for a lot of householders that’s a small decline in contrast with the huge fairness good points lately, there seemingly might be broader results. ANZ Financial institution forecasts subdued shopper spending because of a combination of individuals feeling poorer due to falling home costs, the affect of upper charges on money move, in addition to larger meals and vitality costs, in response to Sharon Zollner, the financial institution’s New Zealand chief economist.

“There are going to be home consumers who’ve simply entered the market within the final 12 months or so who began off with a mortgage charge of two.5 per cent and abruptly they’re rolling off on to a mortgage charge nearer to six per cent,” stated Jarrod Kerr, chief economist at Kiwibank in Auckland. “There’s going to be some ache for positive.” — Ainsley Thomson

CANADA

The housing market in Canada has turned so quick some consumers are shedding cash on their properties earlier than the gross sales even shut.

“Persons are actively attempting to get out of offers,” stated Mark Morris, a Toronto-based actual property lawyer who cited one instance the place a property’s assessed worth got here in $200,000 (US$155,000) lower than the acquisition value agreed to solely a pair months earlier than. That left the client keen to surrender their $100,000 deposit to keep away from closing, he stated. “I’m known as a number of instances a day by numerous individuals who really feel that they’ve paid an excessive amount of.”

Such instances are cropping up after Canada posted its first nationwide home-price decline in two years in April, adopted by one other drop in Could. Although to this point the ache has been concentrated across the markets which noticed the largest pandemic runups — Toronto and its surrounding areas — the strains are already beginning to unfold to previously scorching markets round Vancouver too.

Like in different international locations, the turmoil in Canada’s housing market is being brought on by an aggressive marketing campaign to lift rates of interest by the central financial institution. The benchmark has already gone from 0.25 per cent in the beginning of the 12 months to 1.5 per cent at present. With even larger charges anticipated, some economists say house costs may fall as a lot as 20 per cent within the hottest markets.

It’s a drastic change in a rustic that noticed costs rise by greater than 50 per cent over the 2 years because the pandemic began. With costs quickly outpacing wage progress, some consumers’ hope of coming into the market got here from low charges that are actually leaping.

“It’s the marginal purchaser who’s supporting present valuations, so that might imply important affect on the housing market,” stated Matthieu Arseneau, deputy chief economist at Nationwide Financial institution of Canada, who says house costs nationally may fall as a lot as 10 per cent. “Will new consumers be capable to afford these costs at these charges?” — Ari Altstedter

U.S.

Mabel Melendi may inform the housing market in Cape Coral, Florida, was slowing after every week glided by and she or he nonetheless hadn’t obtained any inquiries or affords on a newly constructed house she listed in mid-April. Simply three months in the past, she obtained a bid on an analogous property inside three days of placing it in the marketplace.

However after three value cuts — knocking the asking value right down to US$425,000 from US$510,000 — and greater than two months after the preliminary itemizing, she was nonetheless searching for consumers in mid-June. One provide that got here in over Memorial Day weekend fell via after the client couldn’t qualify for a big sufficient mortgage.

“The general public don’t qualify for what they used to qualify for earlier than,” Melendi stated.

Mortgage charges have elevated this 12 months on the quickest tempo in data courting again a half century, in response to Freddie Mac. The common charge for a 30-year mortgage reached 5.78 per cent final week, the very best since 2008. That’s led to value cuts for each builders and existing-home sellers as demand quickly cools.

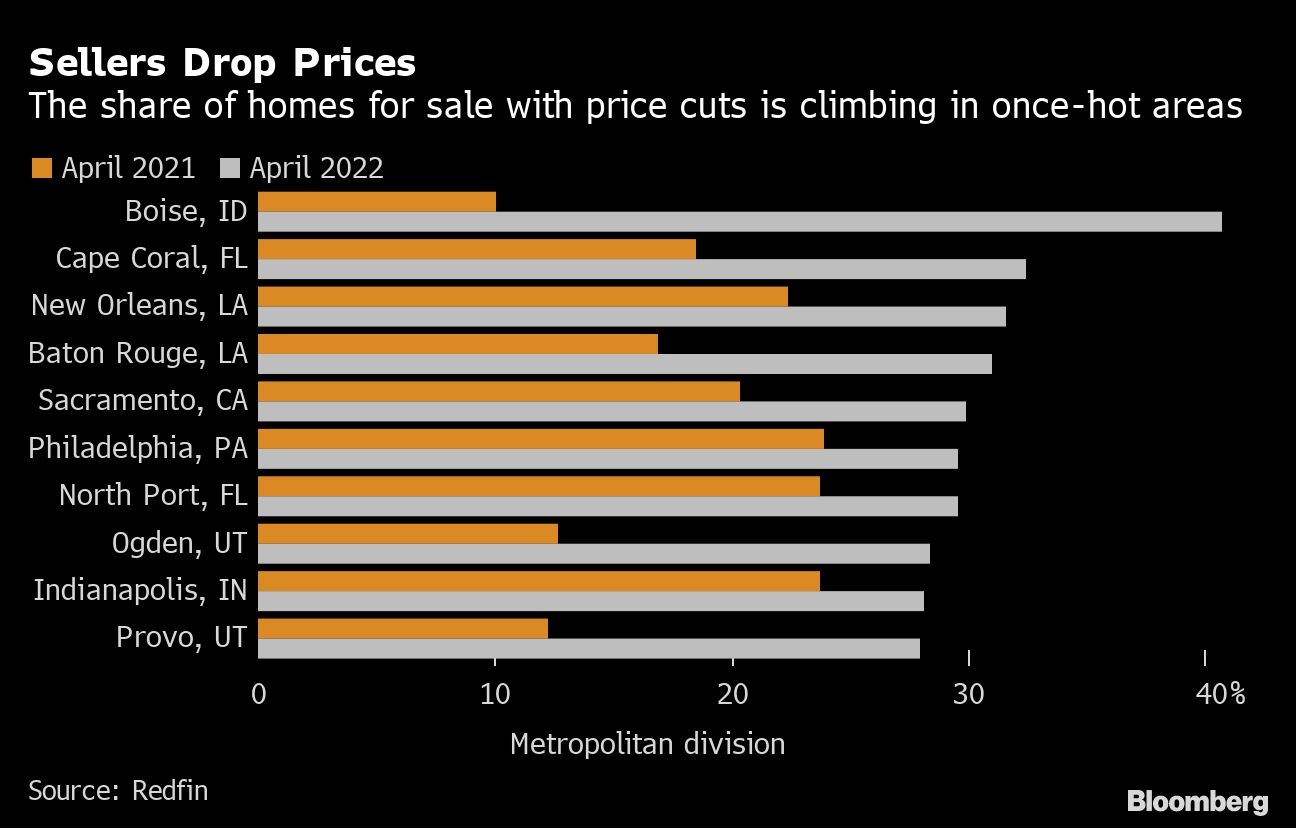

Nearly 20 per cent of US house sellers lower costs within the four-week interval ended Could 22, probably the most since October 2019, in response to the brokerage Redfin Corp. The share was larger in some markets that grew to become scorching locations throughout the pandemic for folks in search of extra affordably-priced houses. In Boise, Idaho, for instance, 41 per cent of sellers dropped costs in April. In Cape Coral, it was about one in three.

Sellers are realizing that costs could not hold rising on the similar tempo they beforehand did as consumers are more and more squeezed, stated Daryl Fairweather, Redfin’s chief economist. “Costs are going to have to come back right down to match demand,” she stated.

After rising by an estimated 18 per cent in 2021, US single-family house costs are forecast to develop by a extra average tempo of 10 per cent in 2022 and 5 per cent in 2023, in response to Freddie Mac. “It’s a reasonably important slowdown, however coming from scorching-hot house-price progress,” stated Len Kiefer, the corporate’s deputy chief economist. A scarcity of houses on the market and pent-up demand from folks in search of more room — together with millennial consumers getting older and beginning households — means costs nationally ought to nonetheless development larger, he stated.

Nonetheless, the results of slowing demand are reverberating via the true property business: Redfin and Compass Inc. stated final week that they’ll lay off workers after the sudden cooldown out there. — Jonnelle Marte

CZECH REPUBLIC AND HUNGARY

The Czech Republic stands out in Europe for its excessive homeownership charge, quick inflation and low unemployment, stated Vit Hradil, a senior economist with Prague-based funding agency Cyrrus. Mixed with a uniquely advanced building allow system and rising demand from expats in search of work within the capital, the nation has confronted staggering value will increase which have far outpaced revenue progress.

A quarterly gauge of Czech home costs rose 26 per cent within the December from the earlier 12 months, in response to London-based knowledge evaluation firm CEIC Information. The distinction between a median citizen’s revenue and actual property costs within the nation is now one of many widest within the European Union, elevating critical bubble fears.

To tame inflation that reached 16 per cent in Could, the Czech central financial institution has been on a financial tightening marketing campaign that lifted rates of interest to the very best degree since 1999, earlier than one other assembly this week.

“You’ll count on these charges to chill demand however, with inflation charges that a lot larger, it’s not working,” stated Hradil, who added that folks within the nation see housing as an inflation hedge and like investing in actual property somewhat than shares.

In Prague, video-effects producer Meera Sankar gave up on shopping for a house. Initially aiming to discover a one-bedroom condominium within the metropolis middle for 3 million koruna (US$130,000), the Eire native finally doubled her funds, however nonetheless couldn’t discover an condominium that met her standards. What she discovered both wanted full renovation or was in a distant or comparatively unsafe space.

“For this type of cash you will get an enormous four-bedroom home close to Cork, Eire, or a 150-square-meter condominium in my dad’s hometown in India,” she stated. “It simply doesn’t add up.”

The Czech Republic ranks second on Bloomberg Economics’ bubble measure, adopted by its regional neighbor, Hungary. There, Prime Minister Viktor Orban has pushed homeownership incentives in a bid to spice up fertility charges.

Costs within the nation elevated virtually 20 per cent within the final three months of 2021, in contrast with the identical interval a 12 months earlier, in response to the European Union’s knowledge company Eurostat. The scenario has solely been exacerbated by the struggle in Ukraine, which has pushed up vitality prices and restricted construction-worker availability. Final week, the central financial institution unexpectedly raised the important thing rate of interest by 50 foundation factors. — Alice Kantor

U.Ok.

The UK housing market is beginning to sluggish after two years of historic progress. As a part of pandemic measures, homebuyers had been exempt from a stamp tax responsibility on properties valued at as much as £500,000 (US$614,000) between July 2020 and June of final 12 months, sending costs escalating even additional and making housing “seemingly indifferent from the remainder of the economic system,” stated Tom Invoice, head of UK residential analysis at Knight Frank.

Now, the Financial institution of England has elevated charges 5 instances in current months, with extra hikes anticipated to come back. That will portend a cooldown in actual property for the remainder of the 12 months, with extra provide changing into accessible as householders rush to beat declines in values, Invoice stated.

Already, approvals for brand new house loans have dropped to the lowest in virtually two years. Purchaser inquiries fell in Could after gaining for eight straight months, in response to a survey from the Royal Establishment of Chartered Surveyors.

“Persons are fearful concerning the economic system, about how the struggle in Ukraine will have an effect on costs and the rising value of residing,” stated Aneisha Beveridge, head of analysis at UK actual property firm Hamptons Worldwide. “They’re extra cautious.”

The Financial institution of England determined this week to scrap affordability assessments, which gauge debtors’ means to repay their mortgages, as of Aug. 1. That would improve the danger of first-time homebuyers making purchases they cannot afford.

Nonetheless, areas corresponding to prime London are faring nicely, Invoice stated, as overseas buyers flock to the worldwide vacation spot and college students return following the pandemic. Secondary cities like Birmingham, Liverpool and Manchester are seeing their costs develop even sooner than within the capital.

“So long as the UK is seen as a rustic with a rule of regulation, good colleges, and the respect of personal property, cash will all the time move in,” Invoice stated. — Alice Kantor

More Stories

Airport Currency Exchange vs Bank Which Offers the Best Rate

Proven Trading Strategies to Navigate Any Market

Emerging Stock Markets Poised for Explosive Growth