Table of Contents

Variable charges might be a get advantages as soon as once more within the midterm

Article content material

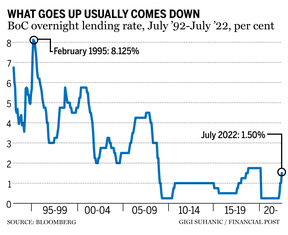

The Financial institution of Canada during the last 30 years has had six sessions of interest-rate hikes, starting from 1.25 to three.2 share issues, earlier than this most up-to-date set in 2022.

Commercial 2

Article content material

The only factor all of them had in commonplace used to be that it didn’t take lengthy for each and every of them to be adopted via a length of declining rates of interest, starting from 1.25 to five.125 share issues.

One logical explanation why for that is that price rises are supposed to decelerate the financial system, and price declines are intended to spice up the financial system. There’s a basic view that the will increase most often get started too overdue, and so charges are nonetheless emerging after the financial system is already slowing. When they in reality begin to take impact, the have an effect on will also be an excessive amount of, and the central financial institution has to do a snappy about-face.

Article content material

Let’s do a snappy assessment of the six rises and falls since 1994.

In October 1994, the Financial institution of Canada’s in a single day price used to be 4.94 in step with cent. Over the following 4 months, it rose considerably to eight.125 in step with cent — a upward thrust of three.2 share issues. Over the next 9 months, it declined to five.94 in step with cent, and twelve months later it used to be sitting at 3 in step with cent. This used to be a big upward thrust and fall traditionally, however it outlines how temporarily charges can upward thrust and the way steep without equal decline will also be.

Commercial 3

Article content material

The following length of price changes noticed the in a single day price upward thrust to five.75 in step with cent from 3 in step with cent over a 15-month length in 1997 and 1998. The following decline wasn’t as steep, however it did drop over the next 9 months to 4.5 in step with cent in Would possibly 1999.

In October 1999, the speed used to be nonetheless 4.5 in step with cent, however then rose to five.75 in step with cent via Would possibly 2000. 12 months later, it used to be again to 4.5 in step with cent and it used to be all of the approach down to 2 in step with cent via January 2002.

Over a 25-month length from March 2002 to April 2004, the speed went from two in step with cent to three.25 in step with cent and again to 2 in step with cent.

All the way through a somewhat wealthy time, the speed rose to 4.5 in step with cent in July 2007 from 2.5 in step with cent in August 2005. However the monetary disaster of 2008 began to rear its head, and charges fell first to 3 in step with cent via April 2008 and all of the solution to 0.25 in step with cent a yr later.

Commercial 4

Article content material

Extra not too long ago, the speed in June 2017 used to be at 0.5 in step with cent, rose to one.75 in step with cent via October 2018, after which dropped to 0.25 in step with cent via March 2020 when COVID-19 started.

What does this imply for nowadays? To this point, we’re 1.25 share issues into an interest-rate-hiking cycle. Some suppose there are every other one or two extra issues in entrance people. Others suppose it’s going to be not up to that. What if the in a single day price is going from 0.25 in step with cent (the place it used to be in February 2022) to two.75 in step with cent? For many people, that may be a foul factor as a result of our borrowing prices can be meaningfully upper. Alternatively, if we have been rather assured that charges would quickly be heading down from there, would that ease our issues?

Historical past suggests this may increasingly occur. The six climbing cycles averaged 13 months in period. The present one is 4 months in. The six declining cycles started on moderate 5.7 months after the hikes stopped, however it came about inside 3 months in 3 of the six eventualities. The typical rate of interest hike used to be 1.95 share issues and the common decline used to be 2.85 share issues.

Commercial 5

Article content material

Historical past could be a information, however in no way a transparent roadmap. If all we did used to be merely have a look at the averages right here, it could counsel that we have got every other 0.7 share issues of price hikes, which might take every other 9 months to achieve. Rates of interest would then begin to decline via September 2023 and sooner or later drop all of the as far back as 0.25 in step with cent (or extra if it used to be imaginable).

In fact, each and every state of affairs is other, so issues received’t merely observe those averages. The reasons are other and the start line on rates of interest is other. That mentioned, this cycle has been very repetitive during the last 30 years.

If I needed to bet, I’d be expecting the rate-hiking timeline can be shorter than 13 months, however that charges will transfer up via extra than simply 0.7 share issues. I imagine the beginning of the speed declines may occur quicker than September 2023. The implied coverage curve for Canada lately means that price hikes will height in six months after which begin to decline with the next yr. This doesn’t imply that this can be a reality, however it displays that even nowadays, the implied coverage price is giving some indication of the similar cycle now we have observed a number of occasions earlier than.

Commercial 6

Article content material

Any other clue as to why the following cycle may appear to be the previous is that even the Financial institution of Canada has mentioned some of the causes for expanding charges is so it’s going to have some better equipment and leverage to assist the financial system via decreasing charges if we move right into a recession or one thing identical.

-

Normalized rates of interest are the treatment, no longer the issue

-

The good normalization has beaten investor sentiment — and that can be an indication the worst is over

-

Fastened-income has been a downturn saviour, however this time is other

If that’s the long term, what does that imply for traders and debtors?

Variable-rate debtors will really feel extra ache within the close to long term, however it isn’t a one-way street. Variable charges might be a get advantages as soon as once more within the midterm.

Commercial 7

Article content material

In case you are having a look at purchasing assured funding certificate, annuities or bonds, it’ll nonetheless be a bit of early to fasten in or make investments, however there might be a candy spot to take action later this yr or within the first part of subsequent yr.

Top inflation and better rates of interest appear to be the most obvious scenario nowadays, however this will likely shift within the not-too-distant long term, so don’t move overboard with this making an investment thesis as it could activate you. You wish to have to be nimble.

The important thing message here’s that we must no longer panic about runaway price hikes. They’ll proceed to upward thrust, however it is usually very most probably that we will be able to see charges fall in a while after the hikes forestall. Possibly this rollover will occur via the tip of this yr or one day in 2023, however being ready for this state of affairs will permit for some funding alternatives and debt alternatives to be maximized.

Ted Rechtshaffen, MBA, CFP, CIM, is president and wealth adviser at TriDelta Monetary, a boutique wealth control company specializing in funding counselling and property making plans. You’ll touch Ted immediately at [email protected].

_____________________________________________________________

For those who like this tale, join the FP Investor Publication.

_____________________________________________________________

More Stories

Portfolio Perfection The Best Way to Diversify Your Investments for Maximum Safety

Investing for Beginners: A Step-by-Step Guide to Grow Wealth

Passive Investing: Grow Wealth Effortlessly